Hosted by Kenneth R. Smith and Jack Monteith

Subscribe to our podcast via iTunes

| Successful Investing Radio Hosted by Kenneth R. Smith and Jack Monteith |

Subscribe to our podcast via iTunes |

|||

|

||||||||||||

|

|

Educational Savings What is the forecast for college cost increases? You've seen the charts--a college education is expensive. All those benefits of personal growth, expanded horizons, and increased lifetime earning power come at a price, a price that increases every year. For the 2006/2007 academic year, the average cost of attendance for a four-year public college is $16,357, while the average cost of attendance for a four-year private college is $33,301. (Source: The College Board's 2006 Trends in College Pricing Report.) The trend of annual college costs outpacing inflation is expected to continue. Why can't colleges keep their prices down? There are many reasons why colleges have a hard time holding down their price increases to the rate of inflation. For one thing, higher education is labor intensive. For another, there are a variety of extra costs that colleges must absorb, like recruiting (these now average over $1,500 per student enrolled at a private college), technology (all those computers and networks), and building maintenance costs. Couple this with the reality that parents increasingly expect more bang for the buck, everything from modernized career centers (so their offspring can find a job after college) to state-of-the-art recreational facilities and medical centers. What expenses are included in the cost of college? In the academic world, the cost of college is generally referred to as the cost of attendance (COA). Each college has its own COA. The COA consists of five items:

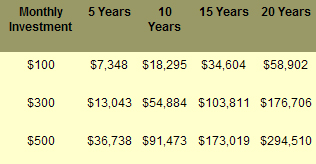

Twice per year, the federal government recalculates the COA for each college and then adjusts the figures for inflation. The government then uses the COA figures to determine your child's particular financial need come financial aid time. Why you should start saving early? Next to buying a home, a college education is the largest expenditure most parents will ever make (and perhaps the biggest expenditure when more than one child is in the family picture). Faced with such a daunting task, you might be inclined to ignore the problem and wait until you are more financially settled before you start saving. But that would be a mistake. The key to sanity in the area of education planning is advance planning. The earlier in the process you become informed about the potential costs and your saving options, the greater chance you will start saving. And the more money you save now, the less money you or your child will need to borrow later. It is important to begin saving as early as possible so you can earn interest, dividends, and/or capital gains on as much money as possible. With a long-term savings strategy, you can hopefully keep ahead of college inflation. Regular investments add up over time. By investing even a small amount of money on a regular basis, you have the potential to accumulate a significant amount in your child's college fund. The following table illustrates how your monthly investment can grow over time (assuming an approximate 8 percent after-tax return rate):

Note: The above example is for illustrative purposes only and does not represent the return of any investment. There is no guarantee that your investment will realize a return and there is a risk that you will lose your investment entirely. How much do you need to save? How much you need to save obviously depends on the estimated cost of college at the time your child is ready to attend. Often, these numbers are staggering. For many parents, the question of how much they should save becomes how much they can afford to save. To determine how much you can afford to save for your child's college each month, you will need to prepare a budget and examine your monthly income and expenses. Don't be discouraged if you can save only a minimal amount at first. The key is to start saving early and consistently, and to add to it whenever you can from raises, bonuses, or unexpected gifts. After you determine how much you can save each month, you will need to choose one or more saving options. There are many possibilities for college savings. To help make your nest egg grow, you will want to maximize the after-tax return on your savings while minimizing risk. Finally, keep in mind that most parents are not able to save 100 percent of their child's college education (after all, do you know anybody who purchased a home entirely with his or her own savings?). Instead, parents generally supplement their savings at college time with a combination of personal loans, financial aid (student loans, grants, scholarships, and work-study), and tax credits to cover college costs.

Copyright 2007 Forefield Inc. All Rights Reserved | ||||

contact@successfulinvestingradio.com |

|||||